Life moves pretty fast

Source: Paramount Pictures

Matthew Broderick, as Ferris Bueller, was talking about paying attention before life runs past you. It applies just as well to money. Financial information now moves quickly and shows up everywhere. Young people are not waiting to be taught. They are already making decisions, using buy-now-pay-later, opening trading accounts, following markets on TikTok and taking cues from whoever speaks most confidently in their feeds. The exposure comes early and often arrives without structure.

That creates a timing problem. Formal financial education, where it exists, tends to arrive later and unevenly. In the United States, more states are introducing personal finance requirements, but rollout is still in progress. In Canada, financial literacy appears across provincial curricula in different ways, with varying depth and consistency. The intent is clear, but delivery is inconsistent and slow to reach everyone. By the time structured education shows up, many young people have already formed bad habits, taken on debt or started making decisions with incomplete information.

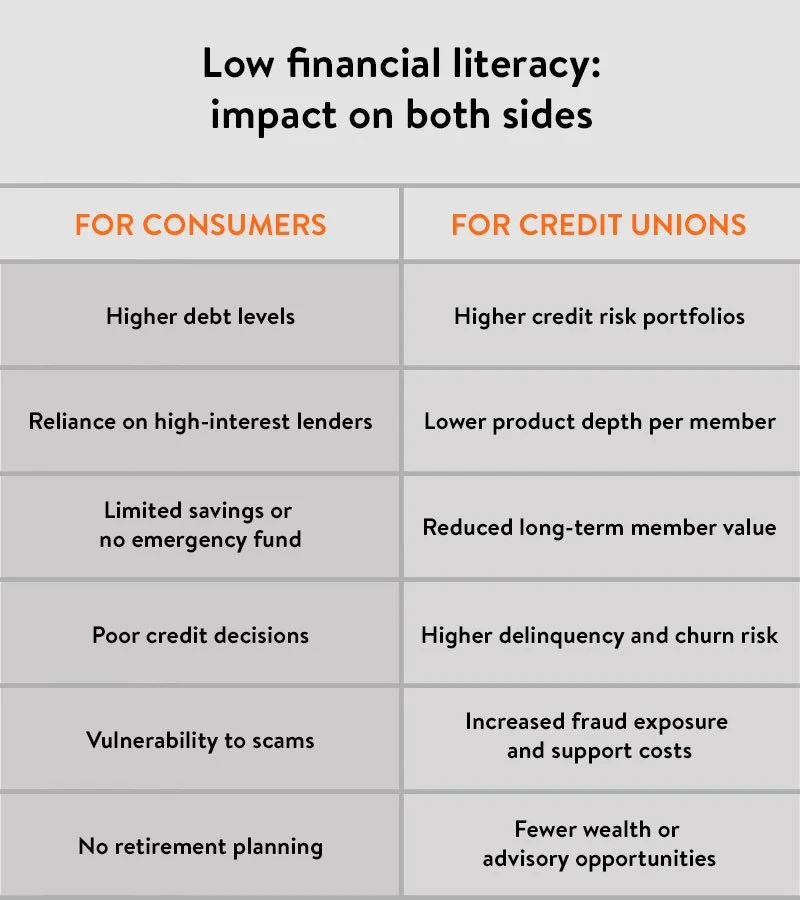

The consequences are easy to see and hard to ignore. Research from Financial Industry Regulatory Authority and Global Financial Literacy Excellence Center shows that roughly half of adults lack a working understanding of basic financial concepts. In practical terms, that shows up as heavier reliance on high-cost credit, limited savings, little in the way of emergency buffers and minimal preparation for retirement. It also leaves people more exposed to financial scams, which are becoming more frequent and more sophisticated.

For credit unions, these patterns show up in how members use products and services. Members with lower levels of financial literacy are more likely to rely on short-term credit, carry persistent balances and have limited savings or financial buffers. Over time, that affects the mix of products held and the stability of member relationships.

From impact to action

For credit unions, this is not a theoretical issue. It shows up in how members use products and services and, over time, in the strength of member relationships. The question is not whether financial literacy matters, but how to deliver it in a way that is consistent and repeatable. That is where most efforts stall. The constraint is not intent. It is coordination, and in practice that tends to delay or dilute delivery.

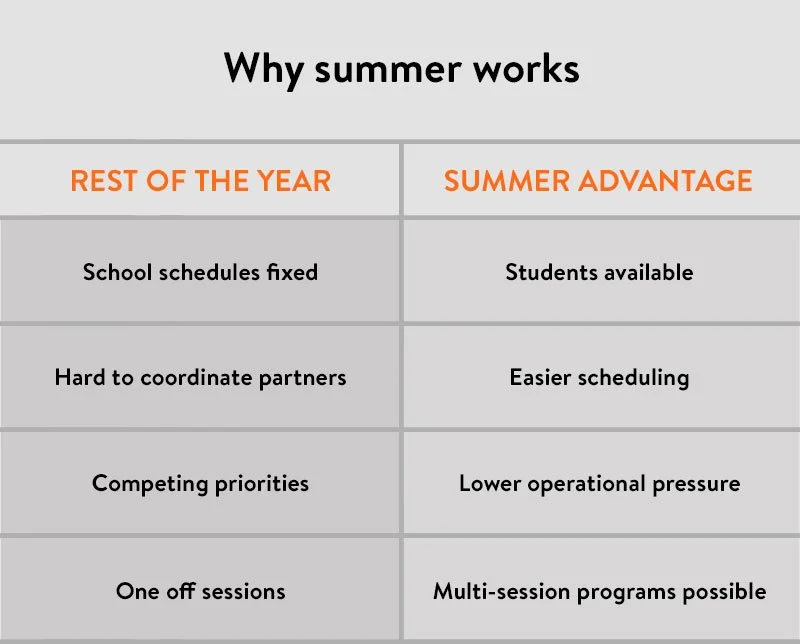

Most credit unions already agree that financial literacy matters. The issue is not intent, it is follow through. Programs are often discussed and supported, but get delayed by scheduling, coordination and day-to-day priorities.

Summer removes much of that friction. Students are out of school, parents are actively looking for structured and useful activities and organizations have more flexibility in scheduling and space. It becomes easier to run something focused and repeatable without the coordination challenges that tend to stall these efforts during the rest of the year.

What is needed at that point is not more content, but a program that can be delivered in a structured and repeatable way.

This is the model behind It’s a Money Thing, now used by more than 100 credit unions across the United States and Canada.

For credit unions, the value is practical. Financial literacy provides a way to engage cohorts that are difficult to reach through traditional marketing, including students, young adults, newcomers and employees. Delivered in schools, community centers or workplaces, these settings become environments where the credit union is present in a useful and relevant role. The cost of access is relatively low and the depth of engagement is significantly higher than most marketing channels.

There is also evidence of downstream impact. Some schools have established student run credit unions operating as micro branches alongside these programs. These initiatives build familiarity with financial services and create early pathways into the credit union. Participating institutions report increased engagement from younger members and, in some cases, recruitment from those same schools.

This is relevant given the demographic pressure many credit unions face. Membership bases tend to skew older, often by close to a decade compared to the general population, while fintech firms continue to capture younger audiences. Financial literacy does not solve that on its own, but it provides a direct way to establish relevance earlier in the member lifecycle.

Annual spend vs. depth of engagement

Most credit unions already invest in community visibility and marketing activity. The question is not whether budget exists, but how effectively it is being used to build meaningful engagement.

Most marketing activity buys attention. Financial literacy earns engagement.

Credit unions are already spending to reach their communities. Financial literacy offers a different type of return. It creates longer interaction, builds familiarity and positions the credit union at the point where financial behaviors are forming. In that context, it functions less as a campaign and more as an ongoing channel.